Have you got enough food in your bunker?

- Anthony Kavanagh, Portfolio Manager

- Mar 17, 2022

- 16 min read

The main facts in human life are five: birth, food, sleep, love and death, E M Forster

It is one thing to run out of cars and have to wait a few extra months for your new Volvo but what happens if we run out of food? A sensationalist comment we agree and virtually unfathomable in the western world but a stark reality for billions of people globally.

A recurring theme since the onset of COVID has been the robustness (and fragility) of global supply chains and with battle lines drawn there is a heightened focus on securing the world’s most strategic resources. The global dominance in semi-conductors is a well-documented motivation in China’s attempts to “unify” Taiwan but as Russian troops intensify their assault on Ukraine we and the rest of the world are asking what are Russia’s or namely Putin’s key motives?

In the past few weeks, we have all seen some of the hard commodity exposures of Russia and Ukraine impacted by the current invasion. I.e., Russia produces: >10% of global oil at 11 mmbbl/d (7.8 of which is exported), ~22.5Tcf p.a. of gas (~40% of Europe’s needs), ~400Mtpa of coal (6th largest coal producer globally), 3.8Mtpa of aluminium (~6% of world production), 920ktpa of refined copper (~4% of world total), 193ktpa of refined nickel (~7% of global production), 40% of global palladium at 2.6Moz and about 90% of global neon production which is used for chip lithography. Less documented (initially at least) was the soft commodity exposures impacted by the conflict, but that has changed as wheat and corn prices have surged to record highs. Russia controls ~50Mtpa of key fertilisers: potash, phosphate and nitrogen; representing ~13% of global supply or ~25% of European supply. Combined Russia and Ukraine account for approximately 29% of global wheat exports, 20% of global corn and 80% of world sunflower exports. Prior to the conflict Ukraine supplied ~15% of global corn. It now feels very likely they will miss the key April/May planting season, putting a lot of that supply at risk.

Truth is we don’t know the full extent of Putin’s motives however food security, even if not intentional, has taken on increasing significance as the conflict has ensued. By controlling Ukraine’s food supply, on top of Russia’s, and its strategic energy reserves places the Kremlin in an interesting negotiating position with the rest of Europe. Maybe pre-empting the conflict, in early February Russia announced an ammonium nitrate export ban, in order to “protect” domestic supply, putting a strain on the already tight global fertiliser market. This could significantly impact other growing regions (such as Brazil) who would be trying to increase supply to offset the loss of Ukrainian and (Russian) supply. These events are raw and it’s perhaps early to draw implications on their lasting significance, particularly for a novice on European politics such as myself, but it is abundantly clear that both companies and countries are having to rethink their global commodity and food supply chains, in addition to their defence budgets.

As a reminder, at Chester, we are bottom up stock pickers, but we like to fish in pools with macro tailwinds. One of those pools we have historically gravitated to is agribusiness, or more specifically the theme of feeding the world. With the macro (omicron, inflation, interest rates and now geopolitics) increasingly challenging and our view food supply chains are becoming strategically more valuable we have found it interesting to find some opportunities in the space trading as genuine value stocks (< book and or low double digit multiples) exhibiting catalysts and blue-sky upside that any growth investor would find appealing.

We present 3 examples of these below, within the overall food thematic but underpinned by strong sub-themes. Notably each of these businesses in the past 12 months have provided some form of medium-term guidance/aspirations which in an environment of truly unpredictable trading conditions support a view of potential asymmetric opportunity. Clearly execution is required to unlock the upside, and we may also be misinterpreting management statements, but trading below book value or on discounted multiples, success is certainly not being priced in.

Land Productivity (reduced arable land)

With a rising global population comes increased demand for food, we’ve all got to eat, but as population increases obviously there is an inverse relationship in the land available for cropping. Hence as a world we need increased land productivity and increased yields. The need for increased yields becomes even more apparent if Ukrainian production is removed from the market for an extended period of time. It comes as Yara cuts production in Europe from rising gas prices and is in conflict with many European (and global nations) trying to limit and even eradicate synthetic farm inputs.

Potential exposures:

Elders - ELD

Incitec Pivot - IPL

Nufarm – NUF (refer below)

Nufarm

Nufarm (NUF) is an Australian based chemical company that produces a large range of primarily off-patent crop protection products and has developed a diversified portfolio of seed technologies. Crop protection products include herbicides, phenoxies, fungicides and insecticides which are sold through the Asia Pacific (namely Australia), North America and Europe across over 3,300 registered products.

In the past NUF has struggled with: a stretched balance sheet, tough weather conditions (Australian drought 2017-2019), glyphosate concerns, and a challenging European environment exacerbating the underperformance of acquisitions. However, the sale of Latin America to Sumitomo (Sep 19), strong Australia conditions (2021, 2022) and a potential environment where food security is prioritised over organic farming have potentially turned those headwinds into tailwinds. The momentum of their seed technologies business has also been evident from a range of announcements and management’s aspirational targets, discussed below.

At the February 2022 Investor Day NUF highlighted they are actually exposed to 4 key global agribusiness trends, being: global nutrition, land productivity, sustainable agricultural practices and the rise of sustainable crops. We have listed NUF here as our preferred exposure to the theme of land productivity as it relates to their core business but the blue sky really sits within sustainable crops (Nuseed) which we have also discussed below.

Insight

Potentially a function of a good season and strong soft commodity prices, in February 2022 NUF announced Q1 FY2022 (December Quarter) revenue had grown 36%. Associated with this statement was vague guidance that NUF expects revenue and earnings growth in FY22 with the market now projecting 6% and 9% revenue and EBITDA growth.

Consequently, we performed a review of NUF historic results as well as analysing competitor announcements for potential insights. Historic comparisons are somewhat challenging given changes to reporting periods for NUF and the divestment of LatAm but loosely the historic margins for NUF are tabled below and suggest outside of FY2020 a pretty steady gross margin between 26 and 30% and EBITDA margin between 11 and 13%.

Source: NUF financial statements

The 2 industry participants we could find that have reported December Quarter results were UPL Ltd and FMC Corporation. FMC Corporation had even issued a guidance statement for CY2022 of 7% revenue growth, 6% EBITDA growth which has somewhat assisted us in forming views around NUF’s potential FY22 earnings.

Source: Chester Asset Management, NUF announcements, UPL Ltd and FMC announcements

I.e., our projections are ~11% above consensus on revenue and ~7% above consensus on EBITDA but note that there are a wide range of possible outcomes in the current environment.

Sustainable Crops

Sustainable crops really plays into NUF’s Nuseeds business with the 2 key technologies being Carinata and Omega-3, in addition to core seeds (Sorghum, Sunflower and Canola).

Both of these two technologies offer a sustainable cropping solution for a global challenge. By way of background Carinata is a biofuel feedstock grown between main crop rotations to help with the decarbonisation of the planet. It is effectively a sustainable alternative to inputs such as diesel and aviation fuel which in itself is a 57bn gallon annual market. Importantly it is a non GMO plant protein source. Nuseed’s Omega-3 Canola solution has been developed as the world’s first land based source of DHA essential ingredients, currently derived from fish oil. Hence this Omega 3 solution has the potential to relieve the pressure on our oceans and reduce the number of fish required to supply the world’s demands for Omega-3, believed to be in material deficit. The Omega-3 canola is processed into 2 oil ingredients: Aquaterra for aquafeed and Nutriterra for human nutrition. NUF estimates the market supports AUD850m EBITDA future market potential i.e., each 1% share of the deficit could be worth AUD8.5m EBITDA.

The ‘aspirations’ of the Nuseeds business were recently defined at the investor day, to grow Nuseed revenues to AUD600-700m by 2026 and AUD1.5bn by 2030 at 25-30% margins.

The targets for Omega-3 have been around for a while but adding Carinata into the portfolio mix is somewhat new and there are a few recent developments that we see providing validation to the commercial prospects of both technologies:

Omega 3 – In addition to USDA and CAN regulatory approvals FDA has recognised Nutriterra as a safe new dietary ingredient. Commercial orders have commenced and NUF recently announced that AUD30m of sales orders had been achieved

Carinata – Nuseed announced a long term commercial offtake and market agreement with none other than BP, providing funding and marketing for Carinata development

Valuation

We most recently re-entered NUF in October 2021 when the stock was trading at ~AUD4.50/share or ~80% of book value, which compares to our current DCF derived valuation of ~AUD6.40/share (WACC10%).

There are 2 key points with our valuation that we point out

a) It includes a heavily risked valuation for Nuseed, that we suspect will derisk over time

b) We have discounted the whole business at the same cost of capital however we believe ultimately the Nuseed business deserves to trade at a higher multiple given the proprietary nature of technology and stronger growth potential than the core crop protection business.

These 2 points are addressed in our alternative valuation scenario tabled below, based on management’s aspirational targets, (which are not guidance statements). They rely on execution, weather and the general range of other uncertainties that come with any projection. However, based on these aspirations, if NUF were to achieve these, under our assumptions there is material upside to the current share price and our risked valuation.

Plant Based Protein

We first wrote about this theme in 2019, with respect to Select Harvest, as Beyond Foods was coming to market (refer a different kind of protein). Today it continues to be one of the fastest growing areas within agribusiness. As of 2021 as many as 6% of US consumers classified themselves as vegan versus 1% in 2014 (1). Australian supermarkets also now offer more than 250 plant based meat products. Hence we think picking a particular brand in this trend may be challenging but taking a “pick and shovels approach” to the theme such as a nut producer or a B2B manufacturer could provide a less risky exposure.

Potential exposures:

GrainCorp - GNC

Select Harvest – SHV (refer previous article)

Synlait Milk - SM1 (refer below)

Synlait Milk

Background

Synlait (SM1 ASX or SML NZX) is a dairy processing company located in Canterbury New Zealand that commenced life as a B2B operator, most famously as the original exclusive infant formula (IMF) manufacturer for A2 Milk (A2M). SM1 controls the supply chain with farmer relationships and processing facilities while also controlling the SAMR (China’s equivalent of the FDA) processing licences on behalf of its customers. Theses licenses are significant as customers such as A2M can’t sell Chinese label IMF into China without them and to highlight their strategic worth it’s important to note that no new SAMR manufacturing licences have been issued globally for the past 3 years.

Over the recent past SM1 has purchased Dairyworks and Talbot Cheese to offer retail brands for the first time and diversify their product offering.

SM1 now offers products across 4 key product lines: Ingredients (whole and skim milk powder and milk fat products), Nutritionals (predominantly infant formula and lactoferrin), Liquids (exciting opportunities in long life consumer packaged beverages and ready to feed infant formula) and Consumer Foods (manufacturing fresh milk, cheese, butter and yoghurt products) under their own or private label brands.

As noted above SM1 has been the exclusive supplier of IMF for A2M in Australia, NZ and China with a contracted minimum 5 year term, while A2M has also cemented the long term arrangement with SM1 by holding a 19.9% stake in SM1.

Plant Based Protein Insight:

Over the past few years SM1 has been on a trajectory to diversify away from an overreliance on their key customer A2M, investing in a liquid’s facility, acquiring consumer goods businesses Talbot Cheese and Dairyworks and entering a relationship with an unnamed customer (2) to manufacture, blend and package nutrition products including plant based products at their site in Pokeno.

This diversification strategy has been somewhat vindicated by the painful results of the past 2 years, exacerbated by volatility in A2M inventory management and planning. This led to a “Bull-Whip Effect” in FY21 of an unforeseen curtailment of A2M IMF production leading to unrecovered overheads and unoptimized production levels i.e., significant losses.

In FY22 Management are anticipating a return to “robust profitability” from a horrible FY21 loss of NZD29m. Furthermore, SM1 has stated that “by the end of FY23, the recovery plan will have seen Synlait return to similar levels of profitability, operating cash flows, and debt ratios as the years leading into FY21”. Despite this optimistic statement SM1 seems to remain friendless.

Famous last words but the worst appears behind SM1 particularly as commercial production of plant based protein for this unnamed customer ramps up later this year. The problem with this agreement however is that the customer and terms are a mystery so it has been a challenge for the market to properly recognise potential value from this agreement (SM1 clearly isn’t Nanosonics).

We have looked at this agreement two ways:

Commentary derived: An estimate based on the commentary around volumes and comparison of historical product margins; and

ROCE approach: Profitability based on capital employed and SM1 generating an acceptable return on that capital commensurate with historic returns, targets and commentary

These two approaches lead us to a guess that this customer could bring in anywhere from NZD30-60m of earnings to SM1 in FY24. It is further expected “volumes, markets and products associated with… (the) agreement will grow over time”.

Source: Chester Asset Management

For SM1 to be trading below book value the market is implying SM1 won’t be able to generate economic returns (> WACC) on capital employed, i.e., assets will remain underutilised. To this end we note the following comments from SM1 in anticipating high levels of utilisation from the Nutritionals business over the next 3 years, driven by:

Some recovery in A2M’s IMF volumes;

New volumes from SM1’s Pokeno customer; and

Rebuild of SM1’s IMF business as demand emerges from large Chinese manufacturers whose market share growth exceeds their own manufacturing capacity

The last point we find extremely interesting for a business that although has multiple customers has production so heavily dominated by A2M. One thing we have learned from years investing with an eye to China is that the Chinese Government follows through on its policies. Hence in 2019 when the government announced they would increase domestic IMF production from ~43% (2018) to 60%, we were cautious to share the market’s scepticism but even we have been surprised as to how quickly they now sit almost at that 60% target(3). Part of the reason for the market’s scepticism was the lack of local manufacturing capacity which obviously hasn’t hindered the progress but is now presenting potential challenges for Chinese producers, particularly if the birth rate goes the way of the Western world post COVID and stops declining! We see SM1 with its strong relationships (Bright, New Hope and other ingredients customers) as well placed (with available capacity) to potentially supply these Chinese customers. Was this image from 12 months ago a teaser to a long term B2B contract?

Source: SM1 1H FY2021 Results Presentation

Valuation

Our assessed value of SM1 currently stands at AUD5.00/share DCF derived (WACC 10%). Chester projections imply 10x FY23 earnings, based on current share price (~AUD3.00/share). Notably net equity stood at NZD3.51/share at 31/7/21, based on net operating assets of NZD1,152m. I.e., SM1 is currently trading below book value.

We see reason why SM1 can trade back towards a ~15x PE multiple as the organic cash flow de-gears the balance sheet and the market regains confidence in their diversified business. If we consider FY23 guidance as returning to a similar level of profitability as the years leading into FY21 we can develop a view as to what that might actually mean for value.

Source: Chester Asset Management, IRESS

I.e., if: a) SM1 is able to return to levels of profitability similar to pre FY21; b) the Pokeno customer is incremental to that profitability and c) SM1 Is able to fortify the longevity of that profitability by entering new LT customer contracts we see a case for SM1 to be valued materially higher.

Pescatarian Diets

This writer has for the past 12 months removed meat from their diet and experimented with pescatarianism with the encouragement from my wife. I.e., I have joined the ~3% of the population that have removed all meat from their diet bar seafood.

This writer is acutely aware that living a sustainable existence would probably also extend to removing seafood from one’s diet but there are arguments that it is a more sustainable source of protein than protein derived from animal farming. Pescatarianism is also arguably seen as a healthier diet than one including meat.

Potential exposures (in addition to plant based protein)

Clean Seas – CSS

Murray Cod - MCA

Ridley – RIC (refer below)

Seafarms Group – SFG

Tassal - TGR

Ridley Corporation

Background

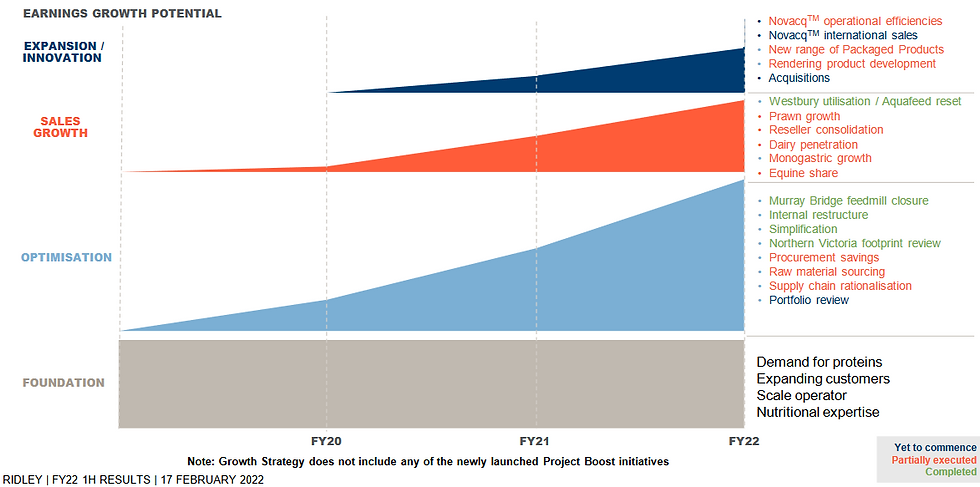

Ridley Corporation (RIC) is Australia’s largest provider of animal nutrition solutions across both bulk stockfeeds and packaged feeds and ingredients across a wide range of monogastric, ruminant, aqua and other species. RIC operates an extensive supply chain throughout eastern and southern Australia with a total capacity of ~1.7Mtpa across 14 feedmills, two rendering sites a packaging site and a supplements facility. RIC also has a number of novel feed opportunities, of which Novacq is the most prominent.

We have seen a marked improvement in the quality of RIC since 2019 that led to us making our investment in the company. In August 2019 Quentin Hildebrand was appointed CEO and MD with Mick McMahon being appointed Chairman the following year as part of a board refresh. We were familiar with Quentin and Mick as the ex COO and CEO of Inghams (ING) a company we had previously invested in. We regard Management and the board highly, sentiment echoed to us by industry contacts.

When Quentin became MD of RIC it had a stretched balance sheet with net debt >AUD140m and leverage >2.5x (ND/EBITDA). Since then, however a marked improvement in working capital management and divestment of their recently constructed extrusion plant in Tasmania, Westbury has led to net debt at 31/12/21 of only AUD17m (0.2x) well below the 1-2x target.

With the change of management in 2019 also came a new “Growth strategy” which management has executed on to optimise return on existing assets, achieve market growth and expand RIC's offering.

Literally using a ruler to estimate the FY22 earnings we measured an AUD82m run rate in FY22 plus potentially an additional AUD9m in Project Boost earnings to flow from FY23 i.e., >AUD90m in FY23 vs ~AUD84m consensus. For 2 years this slide hasn’t really changed hence we believe Management has been extremely transparent and granular and we believe we have witnessed continued outperformance vs targets, a point we felt the market was underappreciating.

We also noted over 12 months ago that the LTIs per RIC’s FY20 Remuneration report had an upper band ROFE target of >30% which we calculated would require >AUD80m earnings by FY2022, a number well north of consensus at the time. This along with our views on management execution has led us to hold an above consensus view on earnings.

Pescatarian Insight

Although we appreciate that RIC is a play on all forms of protein and we see the core business as underappreciated we are also attracted to the upside from their Novacq opportunity. Given the risks evident in investing in aquaculture (TGR and HUO have both almost gone bankrupt in the past) we see Novacq as a novel "picks and shovels" way to play the pescatarian thematic.

By way of background Novacq is a microbial biomass ingredient produced from the use of a carbon waste stream. Novacq was originally developed by the CSIRO in the late 90s and since 2009 RIC has worked with the CSIRO to evaluate the commercial product of Novacq. Essentially it is helping prawns grow bigger (~30%), more sustainably (with less nitrogen discharge), faster and cheaper (with reduced wild fish products in their diets) and with an increased survival rate.

Novacq is still early into its commercial life and its book value was notably written down to zero by management in 2020, but note it has in the past been a key pillar to the RIC story and still represents meaningful upside to the investment case. Despite the FY2020 impairment, in FY2021 RIC tripled production of Novacq from their Thailand site at Chanthaburi and have the business on a pathway to break-even in FY22, after delivering an ~AUD2m loss in the 1H. Notably all 15 Australian prawn customers of RIC have Novacq included in their diet which we see as very strong validation for the product.

Although it is suggested Novacq could be used in diets of species beyond prawns, RIC has previously estimated the total feed market for prawns/shrimp in excess of 6Mt (4) which we now estimate may have grown closer to 8.4Mtpa now, with Ridley licenced in all regions bar China and Vietnam (3rd Party Licenced) to sell the product. This represents ~half of global supply requirements. It is our belief RIC aren’t targeting the whole of this market but rather the early stage lifecycle for prawns, equivalent to maybe 1/6 of the market so ~700ktpa TAM. It is our understanding the Chanthaburi facility in Thailand has current capacity of 30ktpa of Novacq output which could potentially produce 100ktpa of feed at expected Novacq inclusion rates. The facility was originally envisioned to be expandable to 140kt of capacity or 467kt of finished feed capacity (4). We see it likely RIC partner with 3rd parties to assist in the global penetration of Novacq rather than go it alone.

Valuation

At the time of our initial investment in RIC it was trading at ~15x P/E and since that time has delivered:

An improved balance sheet and cash flow conversion, through improved working capital, profitability and the divestment of Westbury;

Growth through strong execution of the 3 year strategy;

Further opportunities for growth including project boost; and

Commercial sales of Novacq demonstrating customer acceptance of the product.

Hence, despite ~30% increase since our initial entry RIC has actually de-rated to ~14x.

Our assessed value of RIC currently stands at ~AUD2.40/share and is based on a DCF of the core business (~AUD2.30/share) plus nominal upside for Novacq.

We could go into detail around our core valuation but thought it more interesting to present a potential upside scenario for Novacq. Unlike SM1’s plant based protein customer and NUF’s Nuseeds business we don’t have commentary with which to base our valuation assessment on however we have trawled through historic releases and formed our own guesstimates to arrive at what we deem a plausible scenario. Given the highly subjective nature of this however we risk it heavily.

Source: Chester Asset Management, IRESS, Various RIC announcements

We further note that although we see this as meaningful blue sky for RIC we are attracted to the valuation appeal of the core business alone and did/ do not see Novacq as a core part of the investment thesis but an area of prospective future upside.

Closing

In these unprecedented times we spare a thought for those genuinely struggling without access to the liberties we are blessed with. We deeply appreciate the value there is in global food supply chains.

(1) View link

(2) We do know from announcements the customer is a “Global category leader in the Asia Pacific region for spray dried and consumer packaged nutritional powder products including plant based proteins. We believe the customer to be Nestle or Danone

(3) View link

(4) View link

DISCLAIMER: Past performance is not a reliable indicator of future performance. Positive returns, which the Chester High Conviction Fund (the Fund) is designed to provide, are different regarding risk and investment profile to index returns. This document is for general information purposes only and does not take into account the specific investment objectives, financial situation or particular needs of any specific individual. As such, before acting on any information contained in this document, individuals should consider whether the information is suitable for their needs. This may involve seeking advice from a qualified financial adviser. Copia Investment Partners Ltd (AFSL 229316, ABN 22 092 872 056) (Copia) is the issuer of the Chester High Conviction Fund. A current PDS is available from Copia located at Level 25, 360 Collins Street, Melbourne Vic 3000, by visiting chesteram.com.au or by calling 1800 442 129 (free call). A person should consider the PDS before deciding whether to acquire or continue to hold an interest in the Fund. Any opinions or recommendations contained in this document are subject to change without notice and Copia is under no obligation to update or keep any information contained in this document current